Fill in Your Michigan Mi 2210 Form

Michigan PDF Templates

Fill in Your Michigan Mi 2210 Form

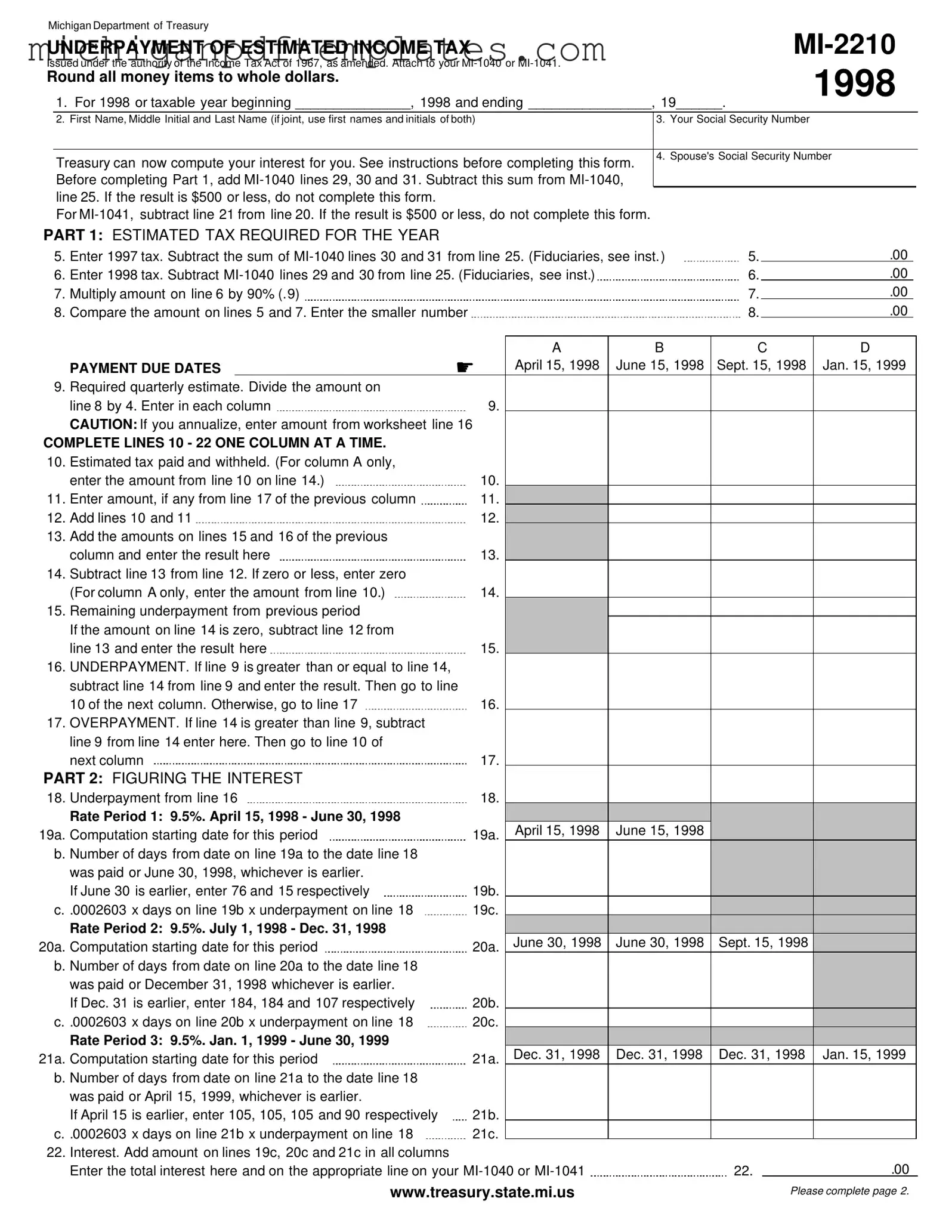

The Michigan MI-2210 form is an essential tool for taxpayers who may have underpaid their estimated income taxes throughout the year. This form, issued by the Michigan Department of Treasury, helps individuals and fiduciaries determine whether they owe any penalties or interest for not meeting their estimated tax payment obligations. When completing the MI-2210, taxpayers will need to provide details about their income, including previous tax amounts and payments made. It requires careful calculations to assess underpayments for each quarter and figure out the applicable interest rates and penalties. The form also offers guidance for those who have uneven income throughout the year, allowing them to annualize their income for more accurate reporting. By attaching the MI-2210 to their MI-1040 or MI-1041, taxpayers can ensure they are compliant with Michigan's tax regulations and avoid any unexpected charges when filing their annual returns.

Understanding the Michigan MI-2210 form is crucial for taxpayers who may be facing penalties or interest due to underpayment of estimated income tax. Unfortunately, several misconceptions can lead to confusion and potentially costly mistakes. Here are six common misconceptions about the MI-2210 form:

This is not true. Even if you expect a refund, you may still need to file this form if you underpaid your estimated tax during the year. Failing to do so can result in penalties and interest.

Timely payment does not absolve you from filing the MI-2210 if your estimated payments were insufficient. The form is designed to assess underpayment penalties, regardless of when you paid your taxes.

While the MI-2210 may seem daunting, it is manageable with careful attention to detail. Following the instructions step-by-step can simplify the process significantly.

This form is applicable to any taxpayer who underpaid their estimated taxes, including individuals. It is not exclusive to business owners or self-employed individuals.

While underpayment may lead to penalties, it is not automatic. The MI-2210 allows you to calculate any penalties owed, and there are exceptions that may prevent penalties from being assessed.

Filing the form does not guarantee immunity from penalties. It is essential to ensure that your estimated payments meet the required thresholds to avoid penalties effectively.

Awareness of these misconceptions can empower taxpayers to navigate the complexities of the MI-2210 form more effectively. Taking the time to understand the requirements can save you from unnecessary penalties and interest in the long run.

Michigan Income Tax Forms - Filing this form assists in ensuring timely processing of tax returns.

New Michigan Auto Insurance Laws - The document includes critical details like the policy number, effective dates, and vehicle identification number.

For individuals seeking to understand the process, the Missouri Mobile Home Bill of Sale document is indispensable for ensuring a smooth transaction. Find out more about how this essential document facilitates the transfer of ownership by visiting this informative resource on the Mobile Home Bill of Sale.

Controlled Drugs Register - Certain types of controlled substances are subject to more stringent tracking measures.

Understand the purpose of the Michigan MI-2210 form. It is used to calculate any penalties and interest for underpayment of estimated income tax.

Before filling out the form, ensure that your total tax liability for the year exceeds $500. If it does not, you do not need to complete this form.

Be aware of the due dates for estimated tax payments: April 15, June 15, September 15, and January 15. Missing these deadlines can result in penalties.

Use the form to compare your actual payments to the required estimated tax. If you underpay, the form helps calculate the interest and penalties owed.

Consider annualizing your income if you receive it unevenly throughout the year. This may help reduce your estimated tax payments.

If you prefer, you can allow the Michigan Treasury to compute your interest and penalties for you. In this case, do not attach the MI-2210 to your tax return.

When filling out the Michigan MI-2210 form, many taxpayers inadvertently make mistakes that can lead to complications or penalties. Here are four common errors to avoid:

Many individuals fail to accurately compute their 1997 and 1998 tax liabilities. It's essential to subtract the correct lines from your MI-1040 form. Double-checking these calculations can prevent unnecessary penalties.

Some filers neglect to consider the $500 threshold for underpayment. If the result from subtracting specific lines on the MI-1040 is $500 or less, you do not need to complete the MI-2210 form. Skipping this step can lead to wasted time and effort.

It's crucial to enter estimated tax payments and withholding amounts accurately. Entering amounts in the wrong columns or failing to account for all payments can lead to incorrect calculations and potential penalties.

If you receive income unevenly throughout the year, you may need to annualize your income. Many taxpayers overlook this requirement, which can affect the accuracy of their estimated payments. Make sure to complete the annualization worksheet if applicable.

By paying attention to these common mistakes, you can help ensure that your MI-2210 form is filled out correctly, minimizing the risk of penalties and complications with your tax return.

Form 1040-ES: This is the estimated tax form for individual taxpayers. Like the MI-2210, it helps individuals calculate and pay estimated taxes throughout the year, ensuring they meet their tax obligations.

Form 2210: This federal form is used to determine if you owe a penalty for underpayment of estimated tax. Similar to the MI-2210, it assesses whether the taxpayer has underpaid their estimated tax and calculates any penalties or interest due.

Form 1041-ES: Designed for estates and trusts, this form allows fiduciaries to make estimated tax payments. It operates similarly to the MI-2210, focusing on the estimated tax obligations of estates and trusts.

Form 4868: This form is used to request an extension of time to file an individual income tax return. While it does not calculate estimated taxes like the MI-2210, it is related in that it deals with tax obligations and deadlines.

Form 1120-W: This is the estimated tax form for corporations. It serves a similar purpose as the MI-2210, helping corporations estimate their tax liabilities and make timely payments throughout the year.

Form 1040X: This form is used to amend a previously filed tax return. While it does not directly relate to estimated payments, it can be used to correct underpayment issues that might be addressed in the MI-2210.

Form 1040-NR: This form is for non-resident aliens to report their income. Similar to the MI-2210, it includes provisions for calculating tax liabilities and estimated payments for those who do not reside in the U.S.

California Motorcycle Bill of Sale: This legal document records the sale and transfer of a motorcycle in California. It ensures the transaction is documented properly, including important details like price and parties involved. For more information, visit legalformspdf.com/.

Form 8862: This form is used to claim the Earned Income Credit after disallowance. While not directly related to estimated tax payments, it can impact overall tax liability, similar to the MI-2210's role in calculating underpayments.

Form 1099: This form reports various types of income other than wages. While it does not calculate estimated taxes, the income reported can affect the estimated tax calculations made on the MI-2210.