Fill in Your Michigan C 8000H Form

Michigan PDF Templates

Fill in Your Michigan C 8000H Form

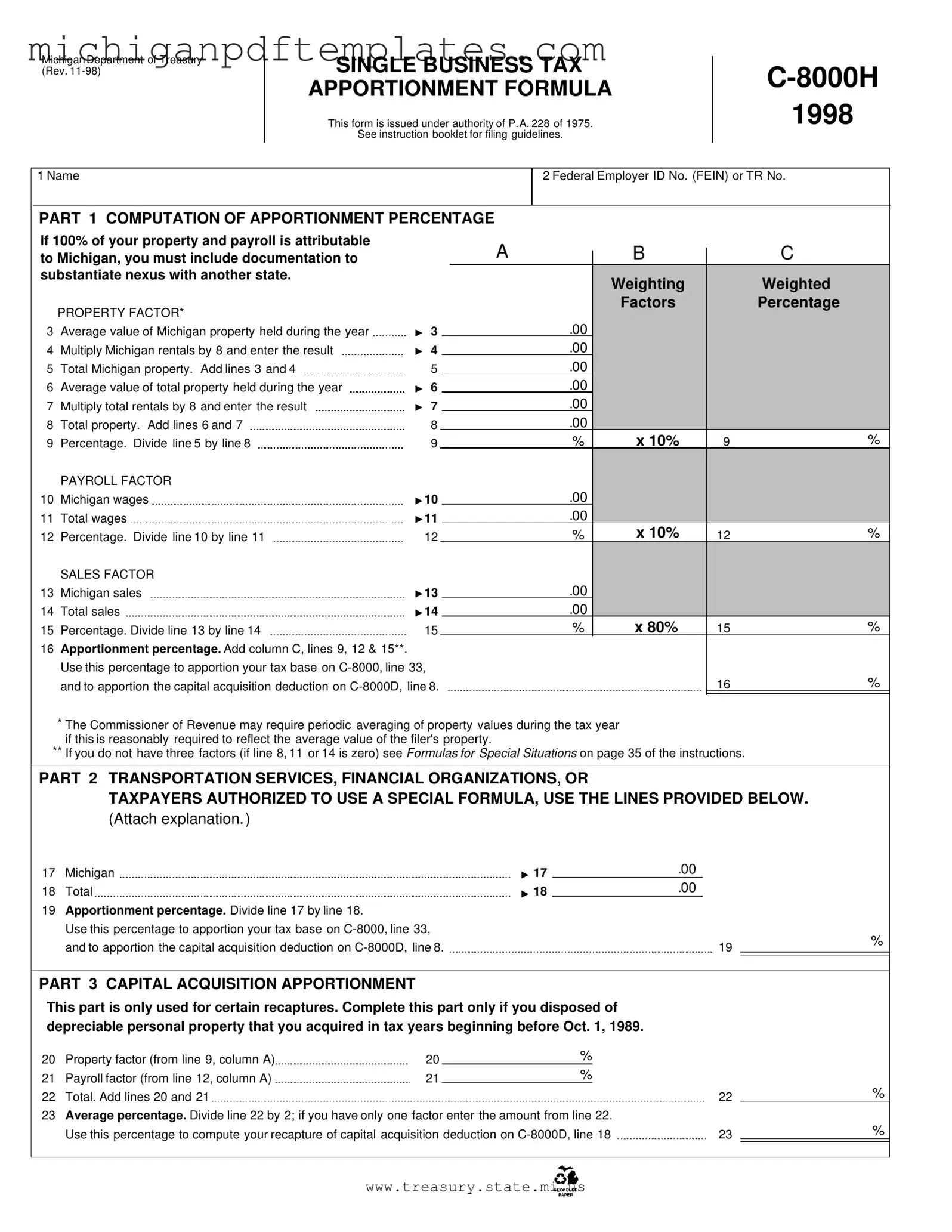

The Michigan C 8000H form plays a crucial role for businesses operating within the state, particularly in determining how to fairly allocate their tax obligations. This form is specifically designed for the Single Business Tax Apportionment Formula, which helps businesses calculate their apportionment percentage based on property, payroll, and sales factors. Understanding this form is essential, as it allows companies to accurately report their financial activities in Michigan while ensuring compliance with state tax laws. The C 8000H includes several parts, each focusing on different aspects of the apportionment process. For instance, Part 1 guides users through the computation of the apportionment percentage by evaluating the average value of property and payroll in Michigan compared to total values. Additionally, it incorporates specific factors that affect the weighting of property and payroll, which ultimately influence the overall tax liability. Other sections of the form address unique situations, such as transportation services or financial organizations that may require a special formula. Furthermore, the form includes provisions for capital acquisition apportionment, particularly for businesses that have disposed of depreciable property acquired before a certain date. Understanding the nuances of the C 8000H form can greatly benefit businesses by ensuring they are meeting their tax obligations accurately and efficiently.

The Michigan C 8000H form can often lead to misunderstandings. Here are four common misconceptions about this form:

Michigan Tax Form - The application encourages a systematic approach to presenting qualifications.

Establishing a Durable Power of Attorney is essential for anyone looking to safeguard their wishes during times of incapacity. By designating a trusted individual to handle important decisions, you can ensure that your preferences are upheld. For residents of Missouri, it's crucial to complete the appropriate documentation, such as the Missouri PDF Forms, to facilitate this process smoothly.

How Does Michigan Unemployment Work - The form asks about the worker's relationship with the employer during the specified calendar year.

How to File a Void Judgement - The applicant must declare there are no outstanding issues regarding the defaulted party's status.

Filling out the Michigan C 8000H form requires careful attention to detail. Here are some key takeaways to consider:

Completing the Michigan C 8000H form accurately is essential for ensuring compliance with state tax regulations. Careful preparation and understanding of the form's requirements can help streamline the process.

Incorrect Federal Employer ID Number (FEIN): Many people mistakenly enter the wrong FEIN or TR No. This number is crucial for identifying your business. Double-check this information to avoid delays.

Missing Documentation for Nexus: If you claim that 100% of your property and payroll is in Michigan, you must provide documentation to prove this. Failing to include this paperwork can lead to complications.

Errors in Property Factor Calculation: When calculating the average value of Michigan property, some individuals forget to include all relevant property. Make sure to account for all property held during the year.

Omitting Special Situations: If you don’t have three factors for your apportionment percentage, you need to refer to the "Formulas for Special Situations." Ignoring this can result in incorrect calculations.

Neglecting to Review the Instructions: Many filers skip the instruction booklet entirely. This booklet contains essential guidelines that can help you avoid mistakes. Take the time to read it carefully.