Fill in Your Michigan 807 Form

Michigan PDF Templates

Fill in Your Michigan 807 Form

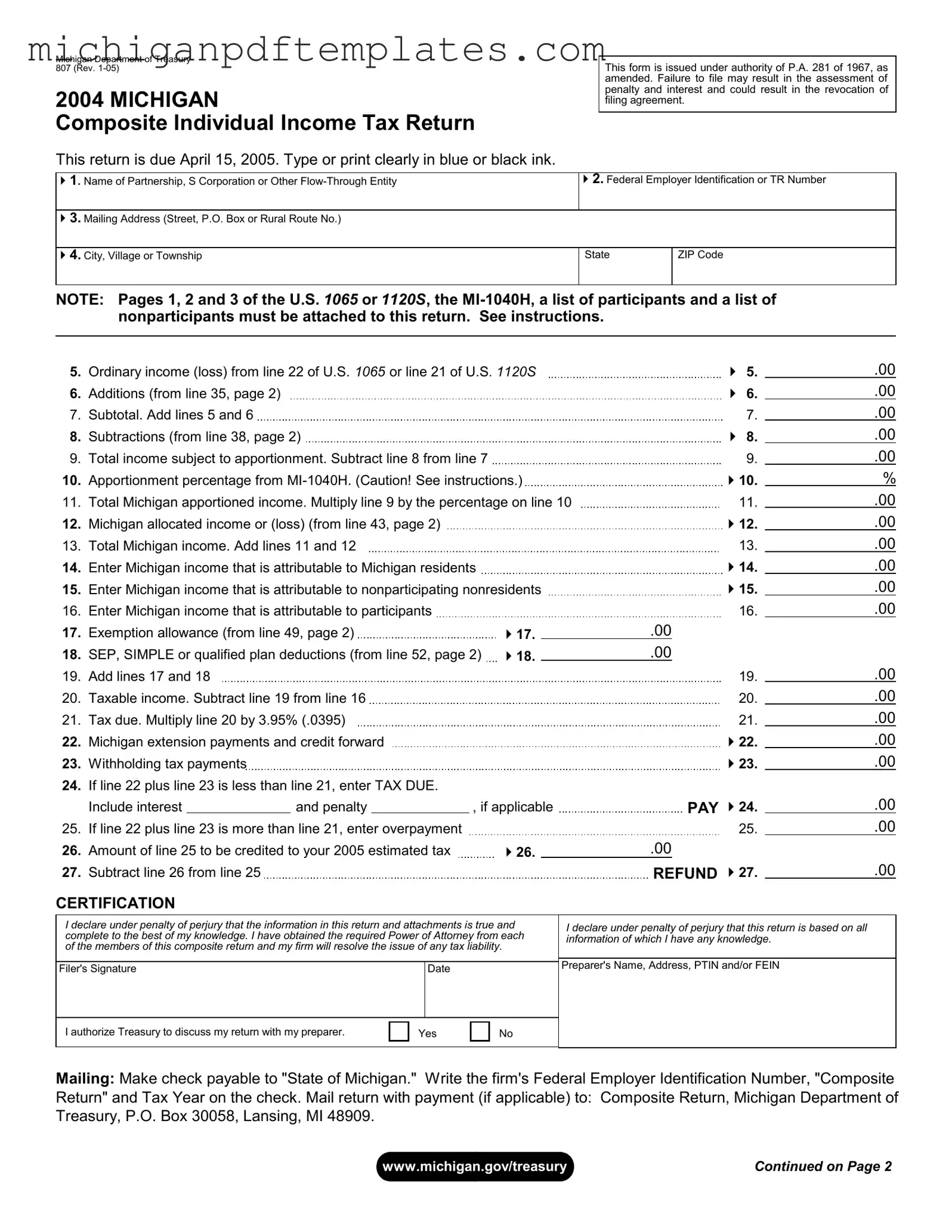

The Michigan 807 form, officially known as the Composite Individual Income Tax Return, is a crucial document for partnerships, S corporations, and other flow-through entities conducting business in Michigan. This form is specifically designed for entities that have two or more nonresident partners, shareholders, or members. Filing the 807 form is essential for compliance with state tax regulations and must be submitted by April 15 of the following year. The form requires detailed information, including the name of the entity, federal identification numbers, and income calculations. Attachments such as the U.S. 1065 or 1120S forms, a Michigan Schedule of Apportionment, and lists of participants are necessary to complete the filing. Key components of the form include sections for reporting ordinary income, additions, subtractions, and determining the total Michigan apportioned income. Additionally, the form outlines the tax due, overpayment, and refund processes, ensuring that all participants are accurately represented and that the entity meets its tax obligations. Failure to file correctly can lead to penalties and interest, making attention to detail vital for those involved.

This form is intended for flow-through entities, which include partnerships, S corporations, and limited liability companies. It is not limited to corporations.

Filing does not automatically result in a refund. The amount of tax owed or refunded depends on the income reported and any applicable deductions or credits.

Not all members can participate. Certain criteria, such as claiming specific tax credits or being a Michigan resident, can disqualify members from participating.

The due date can vary. For example, the 2004 return was due on April 15, 2005. Future returns will have different due dates based on the tax year.

Attachments are required for a complete filing. This includes copies of federal returns and participant lists, among other documents.

Bottle Return Michigan - According to Public Act 148 of 1989, applications must be submitted annually.

Understanding the complexities of the Missouri Compromise is essential for those studying the historical context of slavery in America; for further assistance, you can access the required documentation through the Missouri PDF Forms.

Michigan Sales Tax Exemption - The form emphasizes the importance of proper categorization of sales versus use tax amounts collected.

Michigan Standard Deduction - The Michigan 2271 form is designed for concessionaires to report sales tax in Michigan.

1. Understand the Filing Requirements: The Michigan 807 form is specifically for flow-through entities like partnerships and S corporations with nonresident members. It's essential to ensure that all participants agree to comply with the rules set by the Michigan Department of Treasury. If any participant is claiming certain credits or was a Michigan resident, they cannot be included in this composite return.

2. Timely Submission is Key: The composite return is due on April 15 of the year following the tax period. If additional time is needed, a request for an extension can be made, but it must be submitted before the original due date. Be sure to include any estimated tax payments with the extension request to avoid penalties.

3. Attach Necessary Documentation: When submitting the Michigan 807 form, it's crucial to include several attachments. This includes copies of relevant federal tax forms (U.S. 1065 or 1120S), a Michigan Schedule of Apportionment (Form MI-1040H), and lists detailing each participant’s share of income or loss. Missing documentation can delay processing.

4. Calculate Tax Liability Accurately: The tax due is calculated by multiplying the taxable income by the appropriate rate. It's important to account for any withholding payments made on behalf of nonresident members. If there’s an overpayment, you can choose to credit it towards future estimated taxes or request a refund, but be aware that refunds under $1 will not be issued.

Inaccurate Identification Information: Many individuals fail to provide the correct name of the partnership, S corporation, or other flow-through entity. This information is crucial for proper identification and processing.

Missing Federal Employer Identification Number: Omitting the Federal Employer Identification Number (FEIN) or the TR Number can lead to delays. This number is essential for the IRS and state tax authorities.

Improperly Completed Income Lines: Errors often occur when reporting ordinary income or loss. Ensure that amounts from the U.S. 1065 or U.S. 1120S are accurately transferred to the Michigan 807 form.

Neglecting Required Attachments: Failing to attach necessary documents, such as pages 1, 2, and 3 of the U.S. 1065 or 1120S, can result in processing issues. Always check the instructions for required attachments.

Incorrect Apportionment Percentage: Entering the wrong apportionment percentage from the MI-1040H can lead to significant errors in tax calculations. Double-check this figure before submitting.

Overlooking Signature and Certification: The preparer's signature is mandatory. Without it, the return may be considered incomplete. Ensure that all declarations are signed and dated appropriately.

Improper Payment Instructions: Not following the payment instructions can lead to complications. Make sure to write the firm's FEIN, “Composite Return,” and tax year on the check to avoid processing delays.