Fill in Your Michigan 4816 Form

Michigan PDF Templates

Fill in Your Michigan 4816 Form

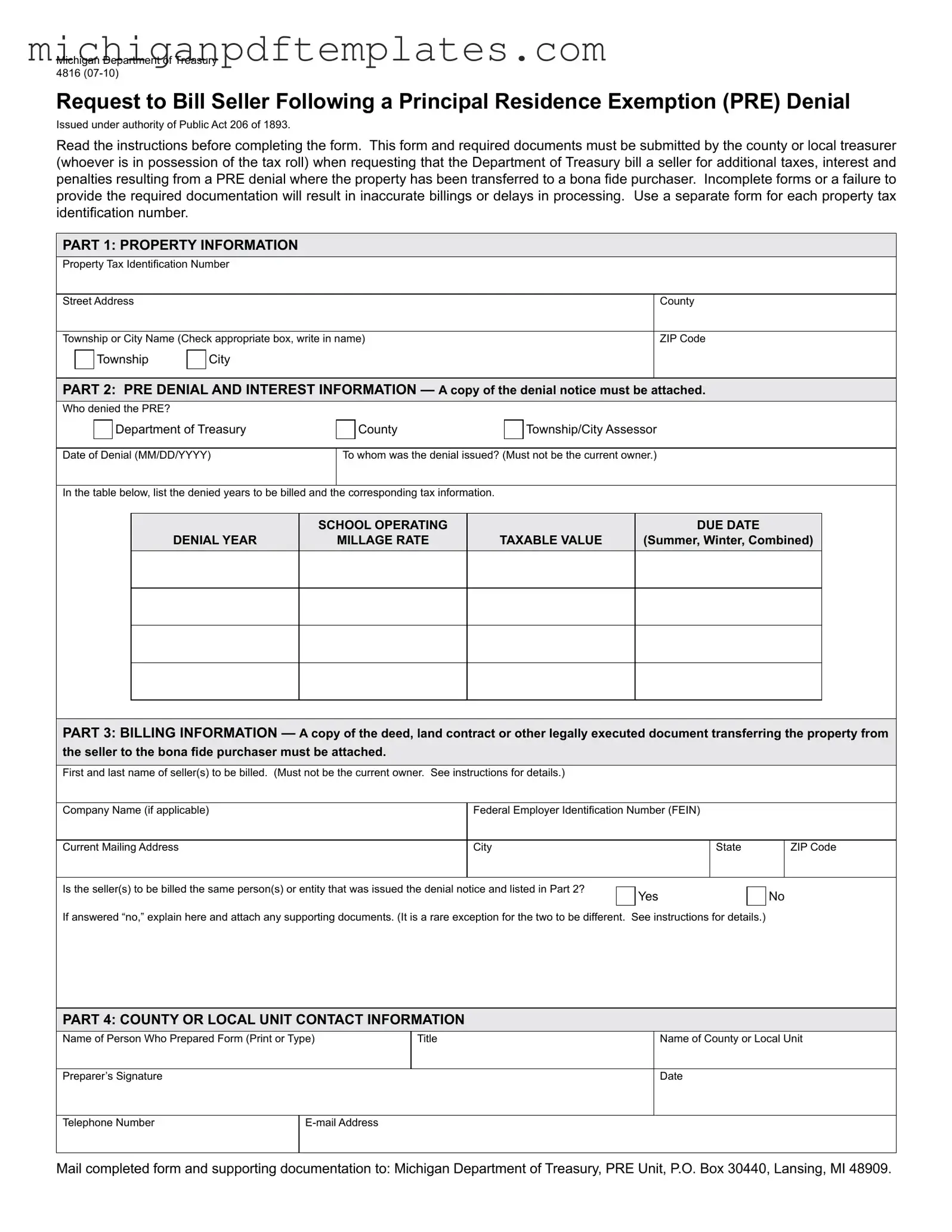

The Michigan 4816 form, officially titled "Request to Bill Seller Following a Principal Residence Exemption (PRE) Denial," serves a critical function in the property tax process within the state. Issued by the Michigan Department of Treasury, this form is utilized when a county or local treasurer seeks to bill a seller for additional taxes, interest, and penalties due to a denial of the PRE. The form must be completed meticulously, as any inaccuracies or omissions can lead to delays in processing or incorrect billing. It is essential to attach required documents, such as the denial notice and proof of property transfer, to ensure the request is valid. The form is divided into several parts, including property information, details surrounding the PRE denial, and billing information for the seller. Each section requires specific data, such as the property tax identification number, the name of the seller, and the circumstances surrounding the denial. The form emphasizes the importance of the bona fide purchaser status, which determines who is liable for the additional taxes resulting from the PRE denial. Understanding the nuances of this form can help property owners navigate potential tax liabilities effectively.

1. The Michigan 4816 form is only for homeowners. This form is actually used by county or local treasurers to bill sellers for additional taxes after a Principal Residence Exemption (PRE) denial.

2. Only the current owner can be billed for taxes. In fact, the seller who received the PRE denial is the one responsible for the additional taxes, not the current owner, if the property was transferred to a bona fide purchaser.

3. You can submit one form for multiple properties. Each property tax identification number requires a separate form. This ensures accurate processing for each property.

4. You don’t need to attach any documents. Required documents, such as the denial notice and the deed or land contract, must be attached. Failure to do so can cause delays or inaccurate billing.

5. The PRE denial is automatically removed upon property sale. The PRE is not removed in bona fide purchaser situations. The seller remains liable for taxes up to the year of sale.

6. Any buyer qualifies as a bona fide purchaser. A bona fide purchaser must buy in good faith for valuable consideration. Inheritances or foreclosures do not meet this criterion.

7. The form can be filled out by anyone. The form must be submitted by the county or local treasurer who is in possession of the tax roll, ensuring proper authority and accountability.

8. You can ignore the due dates listed. It is crucial to include the due dates for the school operating taxes for each denied year. This information is necessary for accurate billing.

9. You can skip the contact information section. Completing the contact information is essential. This allows the Department to reach out for any clarifications or questions regarding the submission.

10. The Department will process the form without any follow-up. The Department will review the completed form and attached documents. Incomplete submissions will result in delays, so thoroughness is important.

Michigan Secretary of State Affidavit Form - The Michigan MV 74 form is designed for individuals seeking an original amateur radio operator call letter license plate.

Waiver Agreement - After filing, the applicant must serve the decision on the other party involved in the case.

In addition to filling out the Missouri Hold Harmless Agreement, it's important to review available resources that can assist you in understanding the legal implications of such documents. One such resource is the Missouri PDF Forms, which offers a variety of forms necessary for your legal needs.

Vacant Land Purchase Agreement Michigan - The seller retains responsibility for property taxes incurred prior to closing, while buyers manage future taxes.

Filling out the Michigan 4816 form can seem daunting, but understanding its key components can make the process smoother. Here are some essential takeaways to keep in mind:

By following these guidelines, you can navigate the Michigan 4816 form with confidence and minimize the chances of delays in processing.

Neglecting to Attach Required Documents: Individuals often forget to include necessary attachments, such as the denial notice or the deed. These documents are essential for processing the request.

Providing Incomplete Property Information: Failing to fill out all sections in Part 1 can lead to delays. Each property tax identification number must be accurately listed, along with the complete address.

Listing Incorrect Denial Information: Some people mistakenly enter the wrong denial date or fail to specify who issued the denial. This can cause confusion and hinder the billing process.

Failing to Specify the Seller: It is crucial to list the correct seller(s) in Part 3. If the seller is not the same person who received the denial notice, this must be explained clearly, along with supporting documents.

Not Using Separate Forms for Different Properties: Individuals sometimes attempt to list multiple properties on a single form. Each property tax identification number requires a separate submission.

Ignoring the Instructions: Skipping the instructions can lead to errors. It is vital to read and understand the guidelines before completing the form to ensure all requirements are met.

Form 4860 - Request for Principal Residence Exemption (PRE): This form is used to apply for a Principal Residence Exemption, which allows homeowners to reduce their property taxes. Like the Michigan 4816 form, it involves property tax identification and requires supporting documentation to be submitted.

Homeschool Letter of Intent: To start homeschooling in Washington, it's essential to complete the necessary documentation, including the hsintentletter.com/washington-homeschool-letter-of-intent-form, which notifies the state of your intent to homeschool and outlines your educational plans.

Form 5040 - Property Transfer Affidavit: This document must be filed when property ownership changes. Similar to the Michigan 4816, it requires details about the property and the parties involved in the transfer, ensuring accurate tax assessment.

Form 5730 - Claim for Exemption from the Property Tax: This form allows property owners to claim exemptions from property taxes. It shares the need for detailed information about the property and the reasons for the exemption, just as the Michigan 4816 does for tax billing after a PRE denial.

Form 5170 - Application for Disabled Veterans Exemption: This form is specifically for veterans seeking property tax exemptions. Like the Michigan 4816, it requires proof of eligibility and supporting documentation to substantiate the claim.

Form 2764 - Notice of Assessment: This document notifies property owners of their assessed property value. It is similar to the Michigan 4816 in that it involves the assessment of property taxes and provides essential information that can affect tax obligations.