Fill in Your Michigan 2796 Form

Michigan PDF Templates

Fill in Your Michigan 2796 Form

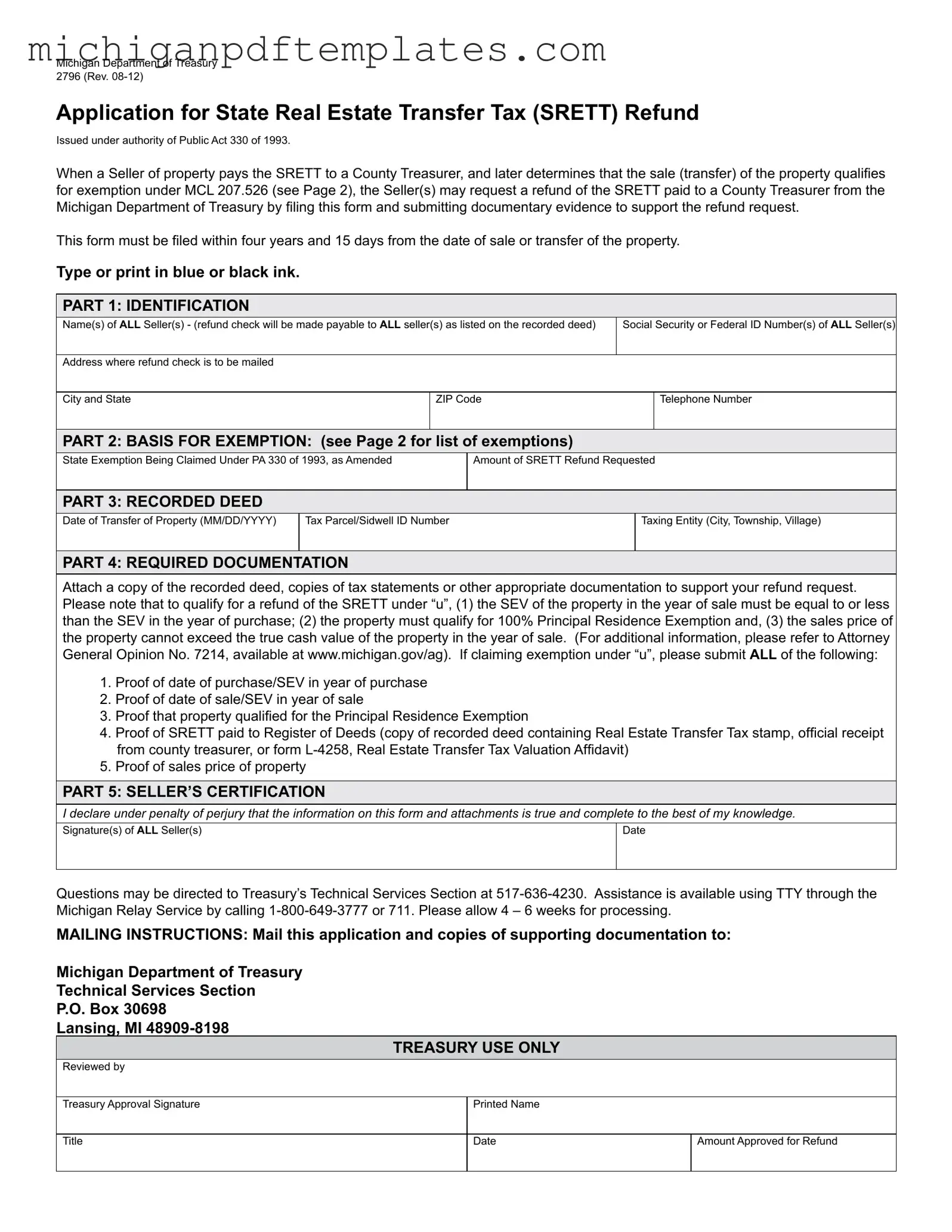

The Michigan Department of Treasury Form 2796, also known as the Application for State Real Estate Transfer Tax (SRETT) Refund, is a vital document for sellers who may be eligible for a refund of the transfer tax they paid during a property sale. Issued under the authority of Public Act 330 of 1993, this form allows sellers to reclaim the SRETT if they find that their property sale qualifies for exemption under specific criteria outlined in Michigan law. To initiate the refund process, sellers must complete the form and submit it along with supporting documentation, including a copy of the recorded deed and tax statements. The request must be filed within four years and 15 days from the date of the property transfer. The form consists of several parts, requiring sellers to provide identification details, specify the exemption being claimed, and detail the transaction's recorded information. Additionally, sellers must certify the accuracy of the information provided, affirming under penalty of perjury that all data is true and complete. Understanding the requirements and exemptions is crucial for sellers to successfully navigate the refund process and ensure compliance with state regulations.

Understanding the Michigan 2796 form can be challenging, especially with the various rules and regulations surrounding it. Here are seven common misconceptions that often lead to confusion:

Many believe there is no deadline for submitting the Michigan 2796 form. In reality, it must be filed within four years and 15 days from the date of sale or transfer of the property.

Some think that only one seller's signature is necessary. However, all sellers listed on the recorded deed must sign the form for it to be valid.

Not every sale is eligible for a refund. The property must meet specific exemption criteria outlined in the form, such as qualifying for the Principal Residence Exemption.

It's a common belief that just claiming an exemption is enough. In fact, you must attach appropriate documentation to support your claim, such as a copy of the recorded deed and proof of taxes paid.

Some assume that the amount of the refund is calculated by the Treasury. However, sellers must specify the amount of the SRETT refund requested on the form.

People often expect immediate processing of their refund requests. In reality, it typically takes 4 to 6 weeks for the Michigan Department of Treasury to process the application.

Many believe that the Michigan 2796 form can be submitted electronically. However, it must be mailed to the Michigan Department of Treasury along with the required documentation.

Being aware of these misconceptions can help streamline the process and ensure that all necessary steps are taken to successfully file for a refund.

Michigan Subpoena Form - Clerk of the court also plays a role in verifying the satisfaction through signature.

To further streamline the process of securing your interests, it is advisable to consult resources like the Missouri PDF Forms that provide necessary documentation for understanding and utilizing the Hold Harmless Agreement effectively.

Waiver Agreement - MC 20 forms are specifically designed for Michigan's probate court proceedings.

Here are some key takeaways regarding the Michigan 2796 form, which is used to apply for a refund of the State Real Estate Transfer Tax (SRETT):

For further assistance, sellers can contact the Treasury’s Technical Services Section or use the Michigan Relay Service for TTY assistance.

Incomplete Seller Information: Failing to provide the names and Social Security or Federal ID numbers of all sellers can delay the processing of the refund request.

Incorrect Mailing Address: Providing an incorrect address for the refund check can result in the check being sent to the wrong location, causing further complications.

Missing Documentation: Not attaching the required documentation, such as the recorded deed or tax statements, can lead to immediate rejection of the application.

Incorrect Exemption Claim: Claiming an exemption that does not apply to the specific situation can result in denial of the refund request.

Failure to Sign: Omitting signatures from all sellers on the form can invalidate the application, as the certification is crucial for processing.

Improper Date Format: Using the wrong date format when entering the date of transfer can create confusion and may lead to processing delays.

Not Filing Within the Deadline: Submitting the form after the four years and 15 days deadline from the date of sale will disqualify the refund request.

Failure to Use Blue or Black Ink: Using a different ink color or writing in pencil can lead to forms being deemed illegible and subsequently rejected.

Inaccurate Tax Parcel/Sidwell ID Number: Entering an incorrect tax parcel or Sidwell ID number can complicate the identification of the property, resulting in delays.

Not Keeping Copies: Failing to retain copies of the submitted form and supporting documents can create issues if follow-up or resubmission is needed.