Fill in Your Michigan 2196 Form

Michigan PDF Templates

Fill in Your Michigan 2196 Form

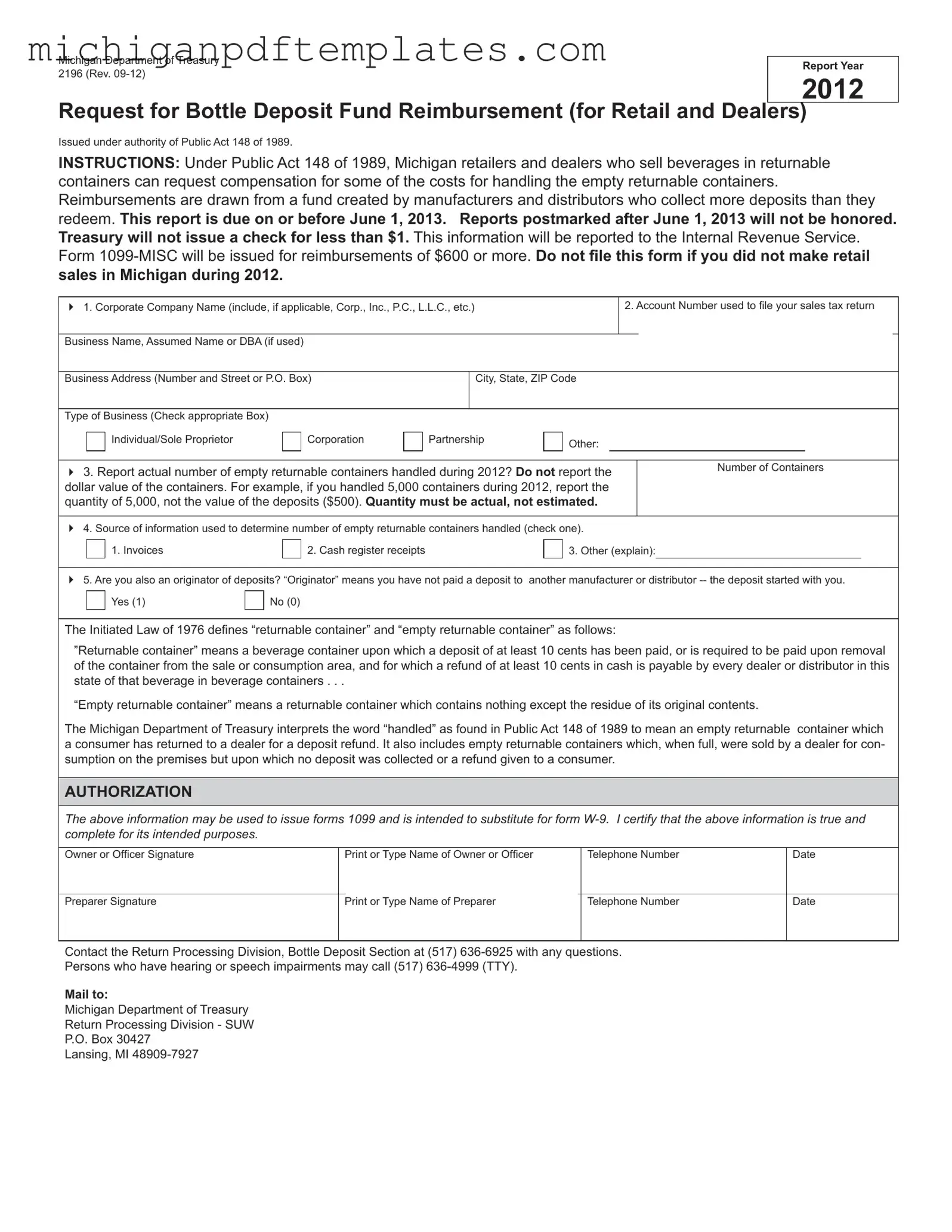

The Michigan 2196 form serves as a crucial tool for retailers and dealers involved in the sale of beverages in returnable containers. This form allows them to request reimbursement for costs incurred while handling empty returnable containers, as outlined by Public Act 148 of 1989. The reimbursement process is funded by manufacturers and distributors who collect more deposits than they redeem, ensuring that those who manage the returnable containers are compensated fairly. It is important to note that this report must be submitted by June 1, 2013, and any late submissions will not be honored. The form requires detailed information, including the actual number of empty returnable containers handled during the reporting year, which must be reported as a quantity rather than a dollar value. Additionally, businesses must confirm whether they are originators of deposits and provide their corporate information. To facilitate accurate reporting, the Michigan Department of Treasury will issue a Form 1099-MISC for reimbursements of $600 or more, and all reported information will also be submitted to the Internal Revenue Service. Retailers and dealers are encouraged to complete the form accurately to ensure timely reimbursement and compliance with state regulations.

Misconception 1: The Michigan 2196 form can be filed anytime.

In reality, the form must be submitted by June 1, 2013. If it is postmarked after this date, it will not be accepted.

Misconception 2: Only large retailers can request reimbursement.

This form is available to all Michigan retailers and dealers who sell beverages in returnable containers, regardless of size.

Misconception 3: You can estimate the number of empty containers handled.

The form requires the actual number of empty returnable containers. Estimates are not acceptable.

Misconception 4: You must pay a deposit to another manufacturer to be eligible.

If you are the originator of the deposits, meaning you have not paid a deposit to another manufacturer or distributor, you can still file the form.

Misconception 5: The reimbursement amount is fixed and known in advance.

The payment amounts depend on how much money is available in the fund, and this is determined by the Treasury after the applications are submitted.

Misconception 6: There is no minimum amount for reimbursement.

The Treasury will not issue a check for less than $1. Therefore, it’s important to ensure your claim meets this threshold.

Misconception 7: The information on the form is confidential and not shared.

The information provided may be reported to the Internal Revenue Service, and a Form 1099-MISC will be issued for reimbursements of $600 or more.

Misconception 8: You can file the form if you did not make retail sales in Michigan during the reporting year.

This is incorrect. If no retail sales were made in Michigan during 2012, you should not file the form.

Misconception 9: Any type of documentation is acceptable to verify the number of containers.

You must provide specific sources of information, such as invoices or cash register receipts, to determine the number of empty returnable containers handled.

Can You Homestead a House You Don't Live in - This form can impact the assessment and tax liability for a homeowner significantly.

Form 4562 Instructions - Part 3 asks for total prepaid revenue or active prepaid account numbers depending on the chosen method.

In light of the importance of legal protections, many individuals choose to utilize resources like the Missouri PDF Forms to ensure their agreements are properly framed and executed, thus minimizing potential liability in various circumstances.

Michigan Permit - Employers are subject to various regulations related to the working hours and conditions of minors.

Here are some key takeaways regarding the Michigan 2196 form:

Make sure to follow these guidelines closely to ensure a smooth reimbursement process.

Incorrect Corporate Name: Failing to include the full legal name of the business, such as Corp., Inc., P.C., or L.L.C., can lead to delays or rejection of the application.

Missing Account Number: Not providing the correct account number used for filing sales tax returns can hinder the processing of the reimbursement request.

Estimating Container Numbers: Reporting estimated quantities of empty returnable containers instead of actual numbers can result in inaccuracies and potential disqualification.

Incorrect Source of Information: Failing to check the appropriate source of information, such as invoices or cash register receipts, may create confusion and complicate the review process.

Not Identifying as an Originator: Neglecting to indicate whether the business is an originator of deposits can lead to misunderstandings about the nature of the transactions.

Missing Signatures: Omitting signatures from both the owner or officer and the preparer can invalidate the form, causing delays in reimbursement.

Form 1099-MISC: This form is used to report miscellaneous income, particularly for payments made to individuals or businesses. Similar to the Michigan 2196 form, it requires accurate reporting of amounts received, especially if they exceed $600. Both forms also necessitate the collection of information about the business or individual involved.

Form W-9: This document is used to request a taxpayer identification number and certification. Like the Michigan 2196 form, it collects essential information about the business entity and certifies the accuracy of that information. Both forms serve as crucial tools for tax reporting.

Sales Tax Return: Retailers use this form to report sales tax collected on sales made during a specific period. Similar to the Michigan 2196, it requires accurate reporting of numbers—whether it be sales figures or the number of returnable containers handled. Both documents are vital for compliance with state tax regulations.

Form 1040 Schedule C: This form is used by sole proprietors to report income or loss from a business. Like the Michigan 2196, it requires detailed reporting of income-related figures, ensuring that all financial data is accurate for tax purposes. Both forms help in determining the financial obligations of the business.

Homeschool Letter of Intent: Parents must submit this form to officially inform the state of their homeschooling intentions. It serves to outline educational plans and to ensure all state regulations are followed. Understanding the criteria for this form is vital for a seamless homeschooling journey in Washington. For more details, visit hsintentletter.com/washington-homeschool-letter-of-intent-form.

Business License Application: This application is necessary for businesses to operate legally within a jurisdiction. Similar to the Michigan 2196 form, it gathers essential information about the business entity, such as name, address, and type of business. Both documents are crucial for establishing legitimacy and compliance with state laws.