Fill in Your Michigan 165 Form

Michigan PDF Templates

Fill in Your Michigan 165 Form

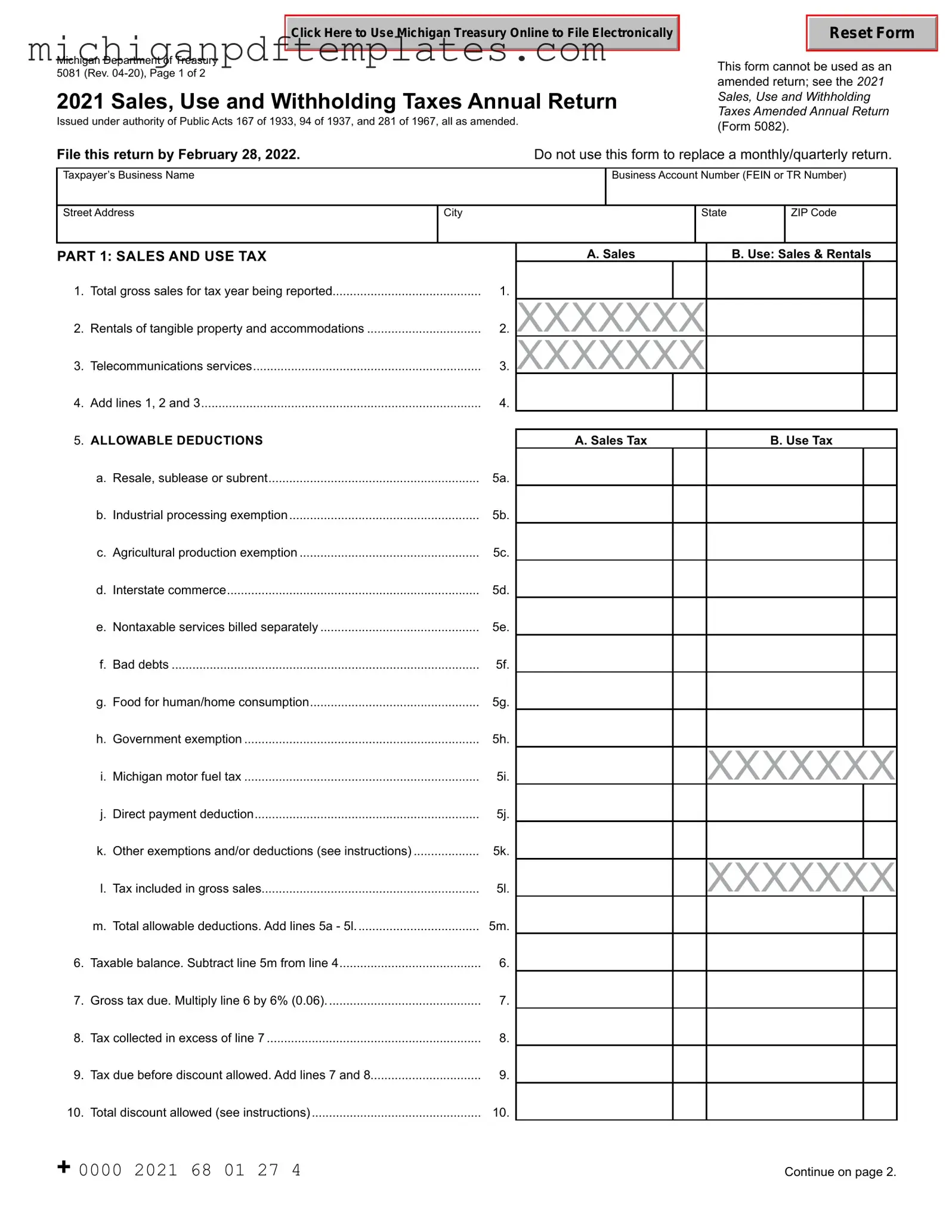

The Michigan 165 form, formally known as the Sales, Use, and Withholding Taxes Annual Return (Form 5081), serves as a crucial document for businesses operating within the state. This form allows taxpayers to report their sales, use, and withholding taxes for the previous year, ensuring compliance with state tax regulations. It is essential for businesses to accurately complete this form, as it encompasses various sections that detail gross sales, allowable deductions, and tax liabilities. The form is divided into several parts, each addressing specific tax categories, including sales and use tax, use tax on items purchased for business or personal use, and withholding tax. Taxpayers must file this return by February 28 of the following year, and it cannot be used as an amended return. Notably, businesses can file electronically through Michigan Treasury Online, simplifying the process and reducing the potential for errors. Understanding the intricacies of the Michigan 165 form is vital for maintaining compliance and ensuring that all tax obligations are met in a timely manner.

Misconceptions about the Michigan 165 form can lead to confusion and errors in tax reporting. Here are ten common misconceptions, along with clarifications to help you understand the form better.

Understanding these misconceptions can help ensure that you complete the Michigan 165 form correctly and avoid potential issues with your tax reporting.

State of Michigan Tax Forms - The designated recipient for this request is Shirley Shananaquet, CMP Administrator.

The Missouri Hold Harmless Agreement form is an essential legal document that helps safeguard one party from liability related to specific actions or events. By ensuring that one party will not hold the other responsible for damages or injuries occurring during certain activities, this agreement is particularly valuable for individuals wanting to mitigate their risks. For those interested in securing their legal standing, a beneficial resource can be found at Missouri PDF Forms.

Michigan Secretary of State Bill of Sale - It’s advisable for applicants to keep a copy of their submitted application for their records.

Mi Form 5080 - The 5092 form must be filled out with corrected figures only, as per the instructions provided.

1. The Michigan 165 form, also known as the 2021 Sales, Use, and Withholding Taxes Annual Return, must be filed by February 28, 2022. Timeliness is crucial to avoid penalties.

2. This form is specifically for reporting sales tax, use tax, and withholding tax. Ensure that you only report taxes for which your business is registered.

3. You cannot use the Michigan 165 form as an amended return. If you need to amend your return, use the 2021 Sales, Use and Withholding Taxes Amended Annual Return (Form 5082).

4. The form allows for electronic filing through Michigan Treasury Online (MTO). This method is encouraged for efficiency and ease.

5. It is essential to provide accurate gross sales figures. This includes all forms of sales, such as cash, credit, and installment transactions.

6. Deductions for nontaxable sales must be substantiated with proper documentation. Keep records of all exempt sales for your business.

7. If you report zero on any line for sales tax, use tax, or withholding tax, you are certifying that no tax is owed. This carries implications if it is later determined that tax is owed.

8. Be aware of the penalties for late filing or payment. A $10 per day penalty applies if the return is filed late, with a maximum of $400.

9. Taxpayers must sign and date the return. If a preparer is used, they must provide their identification number and contact information.

Incorrect Business Information: Failing to provide the correct business name, account number, or address can lead to processing delays.

Missing Signatures: Not signing the form or having the wrong person sign can invalidate the return.

Inaccurate Sales Figures: Reporting incorrect total gross sales can result in underpayment or overpayment of taxes.

Omitting Allowable Deductions: Not claiming all eligible deductions can lead to higher tax liabilities than necessary.

Improper Use of Exemptions: Misapplying exemptions or deductions can cause issues with tax compliance and potential penalties.

Failure to Report Tax Collected: Not reporting tax collected in excess of the amount due can lead to discrepancies and penalties.

Incorrectly Calculating Tax Due: Errors in calculating the taxable balance or gross tax due can result in incorrect payments.

Missing Payment Information: Not including payment details or credits from prior periods can cause confusion and delays.

Ignoring Filing Deadlines: Submitting the form late can incur penalties and interest charges.

Not Using Electronic Filing Options: Choosing not to file electronically when eligible may complicate the process and lead to errors.