Fill in Your Michigan 151 Form

Michigan PDF Templates

Fill in Your Michigan 151 Form

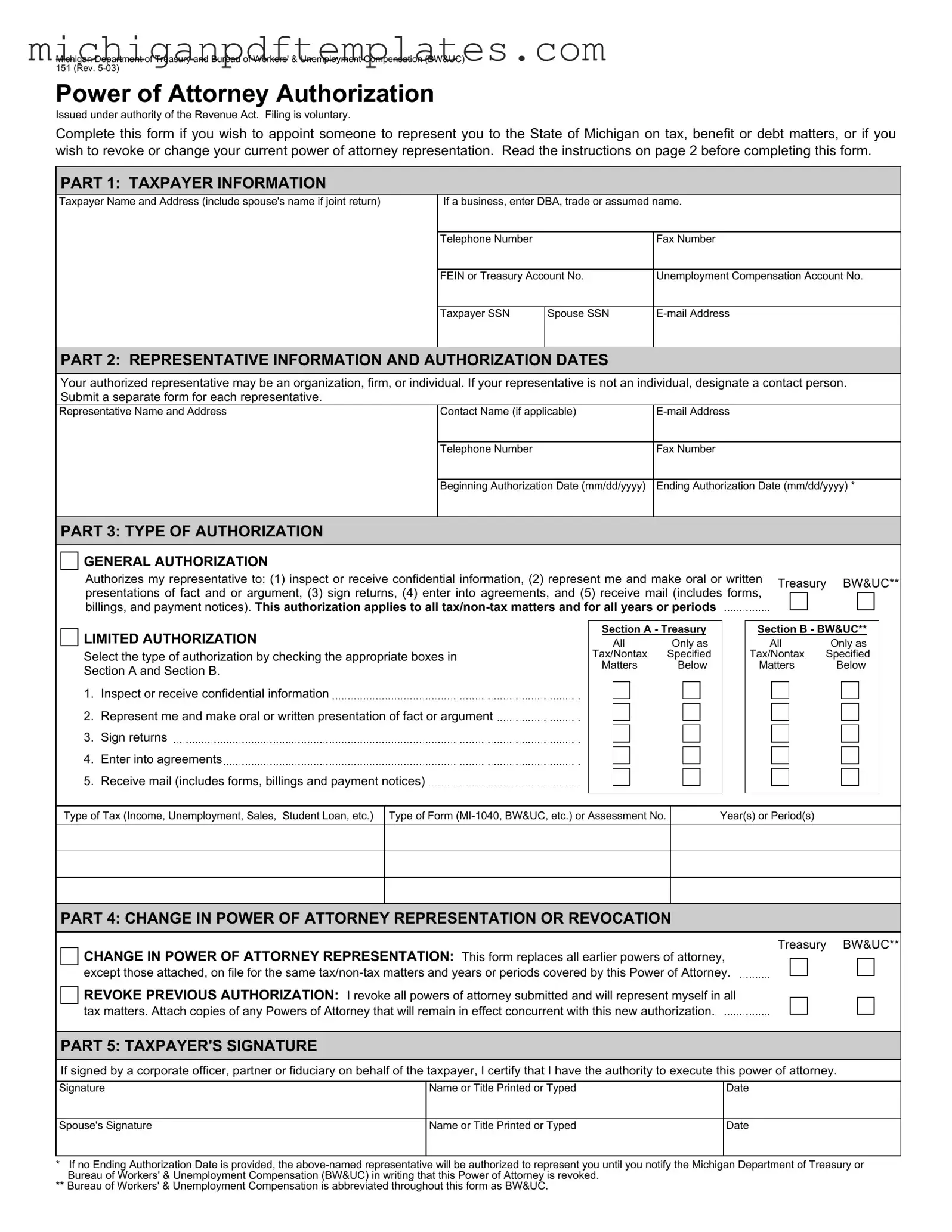

The Michigan 151 form serves as a vital tool for individuals and businesses seeking representation in tax, benefit, or debt matters before the State of Michigan. This form allows taxpayers to appoint a representative—whether an individual, firm, or organization—to act on their behalf. It is important to note that filing this form is voluntary, yet it is essential for ensuring that the Michigan Department of Treasury and the Bureau of Workers' & Unemployment Compensation (BW&UC) can discuss tax-related information with the appointed representative. The form is divided into several parts, starting with taxpayer information, where individuals must provide their name, address, and identification numbers. Following this, the representative's details are captured, including their contact information and the authorization dates. Taxpayers can choose between general or limited authorization, allowing their representative to inspect confidential information, make presentations, sign returns, and receive mail. Additionally, the form includes provisions for changing or revoking existing powers of attorney, ensuring that taxpayers can manage their representation as needed. Finally, the taxpayer's signature is required to validate the form, making it a critical step in securing proper representation in tax matters.

Misconceptions about the Michigan 151 form can lead to confusion and mistakes in the process of appointing a representative for tax matters. Here are five common misconceptions:

Michigan Sales - Use of the form is intended for real estate transactions specifically.

Free Printable Land Contract Forms - This form is crucial for sellers to formally report nonpayment of installments.

For those considering the implications of liability, utilizing a Missouri PDF Forms can be a prudent step. This will aid in comprehensively understanding how the Missouri Hold Harmless Agreement form can shield one party from being held responsible for unforeseen events or damages, ultimately fostering a safer environment in various activities.

Michigan Deed Forms - It serves as an official record to local government about real estate transactions.

Key Takeaways for Filling Out and Using the Michigan 151 Form:

Neglecting to Read Instructions: Failing to read the instructions provided on page 2 can lead to misunderstandings about how to complete the form correctly.

Incorrect Taxpayer Information: Omitting or incorrectly entering the taxpayer's name, address, or Social Security number can cause significant delays in processing.

Missing Spouse Information: For joint returns, forgetting to include the spouse's name and information can invalidate the form.

Improper Authorization Dates: Failing to provide both the beginning and ending authorization dates can result in the form being rejected or misinterpreted.

Choosing the Wrong Type of Authorization: Selecting a general authorization when a limited one is needed, or vice versa, can lead to unintended consequences regarding representation.

Omitting Contact Information: Not providing the representative’s telephone number, fax number, or email address can hinder communication and processing.

Failing to Sign the Form: A lack of signature from both the taxpayer and spouse (if applicable) will render the form invalid.

Not Submitting Separate Forms: If appointing multiple representatives, failing to submit a separate form for each can lead to confusion and delays.

Inadequate Detail for Limited Authorization: Not specifying the type of tax or form when opting for limited authorization can lead to misinterpretation of the powers granted.

Ignoring Previous Authorizations: Not identifying previous powers of attorney that should remain in effect can cause conflicts in representation.

The Michigan 151 form serves as a Power of Attorney Authorization, allowing taxpayers to appoint a representative for tax, benefit, or debt matters. Several other documents share similar purposes and functions. Here’s a look at four of them:

Understanding these documents can help taxpayers navigate their responsibilities and ensure they have the right representation when dealing with tax matters.